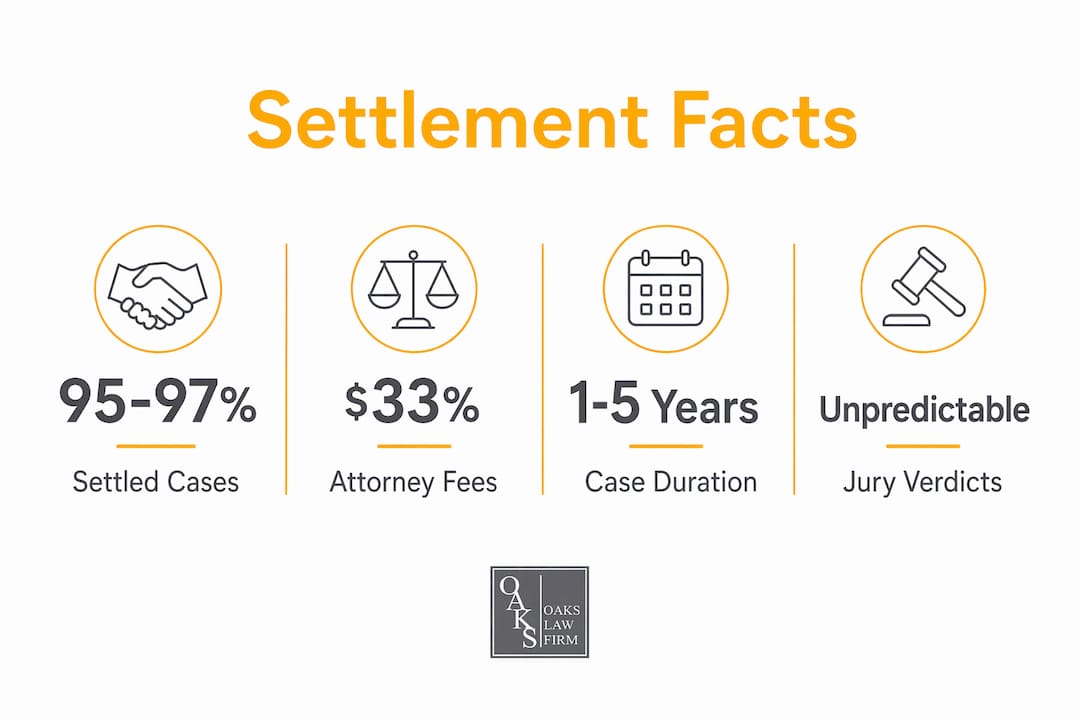

Personal injury cases settle rather than go to trial in 95% to 97% of all claims, making settlement the standard resolution in American civil law, not the exception. The formal term for this process is “pre-trial settlement,” and understanding why personal injury cases settle at this rate tells you everything about how the legal system actually works in practice. Insurance policy limits, the cost of litigation, the unpredictability of juries, and the mutual desire to avoid years of uncertainty all push both sides toward a negotiated agreement. If you are currently involved in a personal injury claim in California, this guide explains the forces shaping your case right now.

Why personal injury cases settle before trial

Settlement is the dominant outcome in personal injury law because it serves the rational self-interest of both parties. The plaintiff gets guaranteed money without waiting years for a verdict. The defendant, usually an insurance company, caps its financial exposure and avoids the risk of a runaway jury award. Neither side enters settlement talks out of weakness. They enter because the math and the risk calculus both point in the same direction.

Trial costs can reach tens of thousands of dollars per side, and a typical personal injury lawsuit lasts one to five years from filing to verdict. A settlement, by contrast, can close a case in months. That time difference matters enormously to an injured person who needs money now to cover medical bills, lost wages, and ongoing treatment. The certainty of a settlement check in hand beats the promise of a larger verdict that may never come, or may be reduced on appeal.

Insurance companies are also sophisticated repeat players in this process. They know that juries are unpredictable, that sympathetic plaintiffs can generate large verdicts, and that prolonged litigation is expensive for them too. Settlement is their preferred tool for managing risk across thousands of claims simultaneously. Understanding this dynamic gives you leverage when you know how to use it.

How insurance limits shape what you can actually recover

Insurance policy limits are the single most important structural factor in settlement negotiations in injury cases. A policy limit is the maximum dollar amount an insurer is contractually obligated to pay on a claim. Once you understand this ceiling, the entire settlement process becomes clearer.

Here is how policy limits work in practice:

- If the at-fault driver carries a $25,000 bodily injury liability policy, the insurer will not pay more than $25,000 regardless of how severe your injuries are.

- If your medical bills total $80,000 and the defendant has no significant personal assets, policy limits cap your recovery at that $25,000 ceiling.

- A jury verdict of $200,000 against an uninsured or underinsured defendant is largely uncollectable if the defendant has no assets to seize.

- Plaintiffs often settle for the full policy limit because it represents the realistic maximum recovery available, not because they are accepting less than their case is worth.

This is why experienced attorneys investigate insurance coverage early. Knowing the defendant’s policy limits tells you the practical ceiling of your case before a single deposition is taken. In California, you can sometimes pursue the defendant’s personal assets beyond their policy, but that requires proving the insurer acted in bad faith or that the defendant has attachable assets worth pursuing.

Pro Tip: Ask your attorney to send a policy limits demand letter early in the process. If the insurer refuses to disclose limits or refuses a reasonable demand within limits, that refusal can become evidence of bad faith and open the door to recovery beyond the policy.

There are strategies to recover beyond policy limits in California, but they require specific legal conditions. Most cases resolve within the available coverage because that is where the money actually exists.

How evidence and risk assessment drive settlement timing

The discovery phase of litigation is where most cases actually settle. Discovery is the formal process of exchanging evidence: depositions, medical records, accident reconstruction reports, and expert witness opinions. What both sides learn during discovery directly determines whether they settle and for how much.

Four factors consistently shift settlement momentum after discovery begins:

- Liability clarity. When surveillance footage, witness statements, or physical evidence clearly establish fault, the defense loses its primary argument. A defendant who cannot credibly dispute liability has every reason to settle quickly.

- Damages documentation. Strong medical records, consistent treatment history, and credible expert testimony on future care needs all increase settlement value. Gaps in treatment or inconsistent records give the defense ammunition to minimize your claim.

- Mutual risk recalibration. After discovery, both sides reassess their exposure. The defense calculates the probability of losing at trial and multiplies it by the likely verdict range. The plaintiff calculates the probability of winning and discounts it by litigation costs and time. When those numbers converge, settlement happens.

- Expert witness credibility. Jurors decide cases based heavily on which expert they find more believable. If your medical expert is compelling and the defense expert is weak, the defense will feel that pressure and move toward settlement.

“Mock trial research shows that strength of evidence and risk recalibration are the primary drivers of settlement decisions, not the emotional state of the parties.” — Legal Clarity Research

Insurance companies now use claims management software like Colossus and Claim IQ to generate initial settlement offers algorithmically. These tools are designed to produce low anchor numbers that feel official and authoritative. Represented claimants receive settlements averaging 3.5 times larger than unrepresented ones, which tells you exactly how much those software-generated offers undervalue legitimate claims. An attorney who understands how these tools work can counter them with targeted medical documentation and negotiation strategy.

Thorough injury documentation from the earliest days after an accident directly affects what the software calculates and what a jury would award. The two are connected.

Why litigation costs and timelines push both sides toward settlement

The financial burden of going to trial is a primary reason why personal injury cases resolve before a courtroom verdict. These costs are real, substantial, and fall on both sides.

| Cost Category | Typical Range | Who Bears It |

|---|---|---|

| Attorney fees (contingency) | ~33% of recovery | Plaintiff (deducted from settlement) |

| Case costs: depositions, filing | 3% to 5% of recovery | Plaintiff (deducted from settlement) |

| Expert witness fees | $5,000 to $50,000+ | Both sides |

| Medical record retrieval | $500 to $3,000 | Plaintiff |

| Trial preparation and exhibits | $10,000 to $100,000+ | Both sides |

The settlement/verdict amount referenced above reflects the specific facts and circumstances of that individual case only. It is not an indication of the value of your potential case, and Oaks Law Firm makes no representation, guarantee, or promise that any future case will produce a similar or comparable result.

After attorney fees of approximately 33% and case costs of 3% to 5%, a plaintiff’s net settlement recovery typically lands between 60% and 70% of the gross amount. Medical liens from health insurers or Medicare can reduce that further by 5% to 20%. This financial reality means that a $100,000 settlement may net the plaintiff $55,000 to $65,000 after all deductions. That number matters when evaluating whether to accept an offer or push for trial.

The emotional cost is equally real. Litigation requires depositions where opposing counsel questions you for hours. It requires reliving the accident, your injuries, and your medical treatment repeatedly over years. Plaintiffs with serious injuries often find that the stress of ongoing litigation delays their psychological recovery. Settlement ends that process on a defined date.

Contingency fee arrangements align attorney and client interests in a specific way. Your attorney earns nothing unless you recover, which motivates aggressive negotiation. But it also means your attorney absorbs the cost of litigation if the case loses at trial. That shared financial risk gives both you and your attorney strong reasons to evaluate settlement offers seriously rather than reflexively rejecting them.

Pro Tip: Before rejecting any settlement offer, ask your attorney to prepare a net recovery analysis showing what you would actually receive after fees, costs, and liens. Compare that number to the realistic net recovery if you win at trial, discounted by the probability of winning.

Why jury unpredictability makes settlement the safer choice

Jury verdicts are the most unpredictable element in personal injury litigation, and that unpredictability motivates settlement on both sides. Jurors’ initial leanings affect verdicts, but deliberations can shift opinions dramatically based on interpersonal dynamics within the jury room that no attorney can control or predict.

Consider what jury unpredictability actually means in practice:

- A plaintiff with severe injuries and clear liability might receive a verdict far below medical expenses if jurors distrust the plaintiff’s demeanor on the stand.

- A defendant with a sympathetic story might win despite strong evidence of negligence, leaving the plaintiff with nothing after years of litigation.

- Conversely, a jury inflamed by egregious defendant conduct might award punitive damages far exceeding what either side anticipated, which then gets reduced on appeal.

- Post-verdict appeals can delay actual payment by one to three additional years, even after a plaintiff wins at trial.

Courtroom verdicts are unpredictable compared to negotiated settlements that guarantee a fixed outcome. Settlement eliminates all of these variables. You know the exact amount, the payment timeline, and the finality of the resolution. For most injured people, that certainty is worth accepting a number below the theoretical maximum a jury might award.

Confidentiality is another factor that drives settlements, particularly in cases involving businesses, employers, or public figures. Defendants often prefer settling with a confidentiality clause over having damaging facts aired in a public trial. That preference gives plaintiffs negotiating leverage they can use to increase the settlement amount in exchange for agreeing to keep terms private.

The decision between lawsuit and settlement ultimately comes down to a risk-adjusted calculation that your attorney should walk you through in detail before you make any final decision.

Key takeaways

Personal injury cases settle because settlement delivers certainty, speed, and financial efficiency that trials cannot match for the vast majority of claimants.

| Point | Details |

|---|---|

| Settlement rate is near-universal | Between 95% and 97% of personal injury cases resolve before trial, making settlement the norm. |

| Insurance limits set the ceiling | Policy limits cap what you can recover regardless of injury severity or jury verdict potential. |

| Discovery triggers settlement momentum | Evidence exchange forces both sides to reassess risk, which is when most serious settlement talks begin. |

| Litigation costs reduce net recovery | Attorney fees, case costs, and medical liens typically reduce gross settlements by 30% to 40%. |

| Jury unpredictability cuts both ways | Neither side can control a jury, making a guaranteed settlement more rational than a speculative verdict. |

What I’ve learned after decades of settlement negotiations

I have handled personal injury cases in California for my entire legal career, and the most consistent mistake I see injured people make is settling too early. Not too quickly in terms of calendar days, but too early in terms of their medical recovery. Settling before you reach maximum medical improvement means you are guessing at future damages. You are estimating surgeries you might need, therapy you might require, and income you might lose. Once you sign a release, that case is closed. You cannot reopen it if your condition worsens.

The second mistake I see is treating the first settlement offer as a starting point for negotiation when it is actually a psychological anchor. Insurance software generates low initial numbers precisely because research shows that anchoring works. People adjust from whatever number they hear first, even when they know that number is artificially low. The right response to a first offer is almost never acceptance. It is a counter-demand backed by documented evidence.

What I find genuinely interesting about 2026 is how data-driven negotiation has become on both sides. Insurers use Colossus and similar tools. Plaintiffs’ attorneys now use case valuation software and verdict databases to benchmark offers against comparable cases in the same jurisdiction. That transparency is good for injured people because it makes low-ball offers harder to defend. An insurer offering $30,000 on a case where comparable verdicts in Los Angeles County average $150,000 has a difficult conversation ahead.

My honest advice: work with an attorney who prepares every case as if it will go to trial, even when settlement is the likely outcome. That preparation is what produces better settlement offers. Insurers know which firms will actually try cases and which ones will fold. That reputation matters more than most people realize.

— Matthew Nezhad

How Oaks Law Firm approaches your settlement

At Oaks Law Firm, Matthew Nezhad and his team prepare every personal injury case with trial-level rigor, which is exactly why insurers take their settlement demands seriously. The firm operates on a contingency fee basis, meaning you pay nothing unless you recover. That model aligns the firm’s interests directly with yours. Whether your case involves a car accident, a slip and fall, or a workplace injury in the San Fernando Valley, the team investigates thoroughly, documents aggressively, and negotiates from a position of strength. If you want to understand how to file a personal injury lawsuit or simply want a realistic evaluation of your settlement options, contact Oaks Law Firm today for a free case evaluation.

FAQ

Why do most personal injury cases settle out of court?

Between 95% and 97% of personal injury cases settle because settlement offers faster resolution, lower costs, and a guaranteed outcome compared to the unpredictability and expense of a jury trial.

What factors most influence a personal injury settlement amount?

Insurance policy limits, the strength of liability evidence, the severity and documentation of injuries, and the jurisdiction’s typical verdict range all directly shape what a settlement offer looks like.

How long does it take to settle a personal injury case?

Settlement timelines range from a few months for straightforward claims to over a year for complex cases. Trials, by comparison, typically take one to five years from filing to verdict.

Should I accept the first settlement offer from an insurance company?

No. First offers from insurers are generated by claims software designed to anchor negotiations at a low number. Represented claimants receive settlements averaging 3.5 times larger than those who negotiate without an attorney.

What happens to my settlement money after fees and costs?

After attorney fees of approximately 33%, case costs of 3% to 5%, and any medical liens, most plaintiffs net between 60% and 70% of the gross settlement amount. Understanding this before accepting an offer is critical to evaluating whether it is truly fair.

This article is provided for general informational purposes only and does not constitute legal advice. The information presented may not reflect the most current legal developments and should not be relied upon as a substitute for consultation with a licensed attorney. Every personal injury case involves unique facts and circumstances, and the outcome of any case depends entirely on those specific facts. Any results, settlement amounts, or verdicts referenced in this content are specific to the individual cases described, are not typical, and do not guarantee, promise, or predict a similar outcome in your case. Reading this content does not create an attorney-client relationship with Oaks Law Firm. Contact us directly for a consultation specific to your situation.