A rideshare accident claim with Uber or Lyft is defined as a legal demand for compensation filed against one or more insurance policies after a collision involving a platform driver. What makes these claims uniquely complex is that the applicable coverage depends entirely on what the driver was doing inside the app at the moment of impact. Filing without understanding that distinction can cost you thousands of dollars in recoverable compensation. This guide explains the insurance periods, the step-by-step filing process, the disputes you will likely face, and the strategies that produce the best outcomes. Oakslawfirm has handled these cases throughout California and sees the same costly mistakes repeated by victims who go it alone.

Disclaimer: This article provides general legal information only. Your specific case facts, jurisdiction, and circumstances may produce different outcomes. Nothing here constitutes legal advice, and you should consult a qualified attorney about your individual situation.

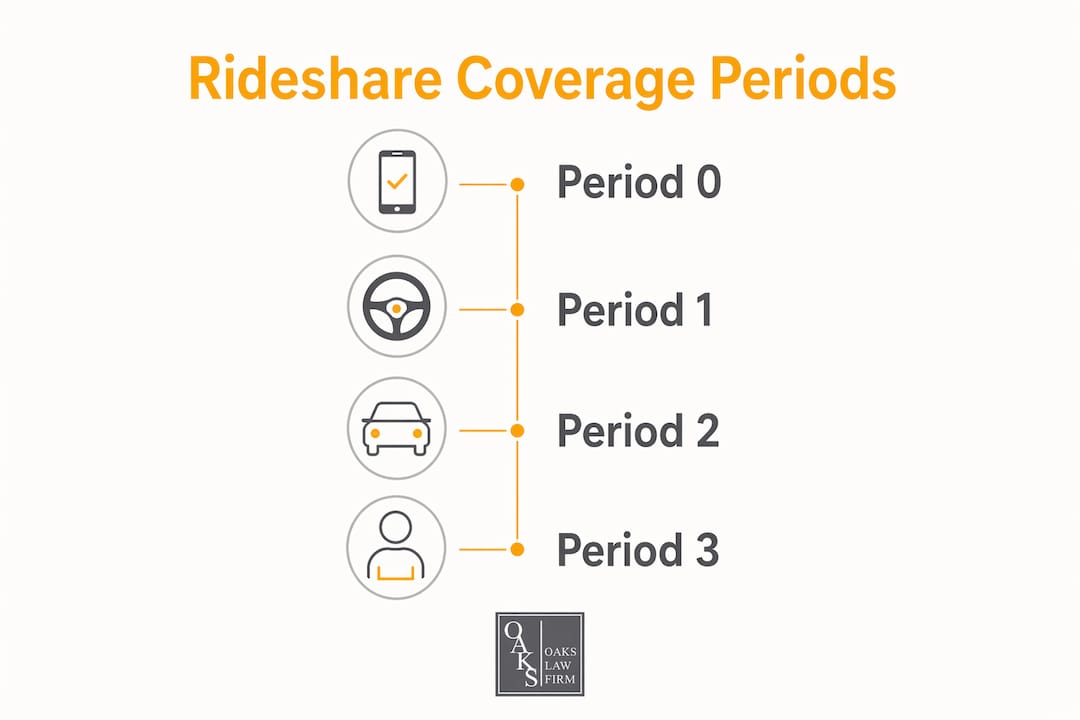

What insurance coverage applies during different rideshare periods?

Rideshare insurance coverage is divided into four distinct periods, and the period active at the time of your accident determines which policy pays and how much. Coverage limits vary dramatically from $50,000 to $1,000,000 depending on app status. That range is not a minor detail. It is the single most important fact in your entire claim.

Period 0: app completely off

When the driver’s app is off, Uber and Lyft carry zero liability. The driver’s personal auto policy is the only coverage available. This is the simplest scenario, and it functions like any standard car accident claim.

Period 1: app on, no ride accepted

Period 1 is where most victims get hurt financially. Personal policies typically exclude commercial use the moment a driver logs into the app, which means the driver’s own insurer can deny the claim outright. Uber and Lyft do provide limited liability coverage during Period 1, with minimums of $50,000 per person and $100,000 per occurrence, but there is no collision or comprehensive protection included. Victims injured during Period 1 face the narrowest coverage window of all four periods.

Periods 2 and 3: active trip

Once a driver accepts a ride request (Period 2) or has a passenger in the vehicle (Period 3), primary commercial liability of $1,000,000 kicks in. This is the most favorable scenario for injured victims. The coverage is primary, meaning it pays before any personal policy.

California’s SB 371 places a cap on uninsured and underinsured motorist (UM/UIM) coverage at $60,000 in certain situations. That cap matters when the at-fault driver carries minimal insurance and you are trying to recover the full value of your injuries.

| App Period | Driver Status | Liability Coverage | UM/UIM Available |

|---|---|---|---|

| Period 0 | App off | Personal policy only | Personal policy only |

| Period 1 | App on, no trip | $50,000/$100,000 (platform) | Limited or none |

| Period 2 | Trip accepted | $1,000,000 primary commercial | Yes, subject to SB 371 cap |

| Period 3 | Passenger in vehicle | $1,000,000 primary commercial | Yes, subject to SB 371 cap |

Pro Tip: Screenshot the ride receipt and your trip status confirmation immediately after any accident. That single piece of evidence establishes which coverage period applies and prevents the insurer from later disputing the driver’s app status.

Rideshare endorsements on personal policies cost roughly $15–$40 per month and fill the Period 1 gap, but most drivers do not carry them. That gap in driver coverage directly affects how much you can recover as a victim.

How do you file a rideshare accident claim with Uber or Lyft?

Filing a rideshare accident claim follows a specific sequence. Skipping steps or doing them out of order weakens your case before it even reaches an adjuster.

Immediate actions at the scene

- Call 911 and get medical attention, even if injuries feel minor. Delayed symptom onset is common in soft-tissue injuries.

- Request a police report and get the report number before leaving the scene.

- Photograph the vehicles, road conditions, traffic signals, and any visible injuries.

- Screenshot your Uber or Lyft app to confirm the trip was active and capture the driver’s name, vehicle, and trip ID.

- Collect contact information from all witnesses present.

- Do not give a recorded statement to any insurance adjuster at the scene.

Reporting to Uber or Lyft

- Open the app and navigate to your trip history to find the specific ride.

- Use the in-app help feature to report a safety incident or accident.

- Uber routes serious accident reports to its Critical Safety Response team. Lyft uses a similar internal process.

- Both platforms will ask for a description of the incident. Keep your statement factual and brief.

Documentation to gather

- Medical records and bills from every provider you visit.

- Written confirmation of the driver’s app status from the platform (request this in writing).

- Photos and video from the scene.

- Witness statements, preferably in writing.

- Proof of lost wages if the injury kept you from work.

Pro Tip: Request a copy of the police report within 10 days of the accident. Insurance adjusters use it as a baseline for fault determination, and errors in the report can be corrected while the details are still fresh.

Uber and Lyft both include arbitration clauses in their terms of service. Those clauses can limit your ability to sue in civil court and require disputes to be resolved through a private arbitration process. An attorney can review whether the clause applies to your specific claim and whether any exceptions exist.

What are the most common disputes in rideshare accident claims?

Insurers frequently challenge claims by disputing the driver’s app status at the exact moment of the accident. That dispute alone can shift your claim from $1,000,000 in primary commercial coverage down to a personal policy that may deny the claim entirely. This is the most common tactic, and it catches victims off guard.

- App status disputes: The insurer argues the driver was between trips or had logged out seconds before the crash. Without documented proof of trip status, this argument is hard to counter.

- Coverage layering conflicts: Personal insurers and platform insurers each point at the other as the primary payer. Claims stall while both sides negotiate responsibility.

- Medical and health plan liens: Medicare, Medicaid, ERISA health plans, and hospital liens all reduce your net settlement. Victims often receive far less than the gross settlement figure after lien deductions.

- High deductibles on contingent collision coverage: Platform collision coverage carries a deductible of around $2,500, and it only applies if the driver personally carries collision and comprehensive on their own policy. Many drivers do not.

- Arbitration complexity: If your claim proceeds to arbitration, the rules differ significantly from civil court. Discovery is limited, and the arbitrator’s decision is usually final.

“Rideshare accident claims are not standard car accident cases. The layered insurance structure, app-period disputes, and lien resolution requirements make them among the most technically complex personal injury claims in California. Victims who handle these claims without legal counsel routinely leave significant compensation on the table.”

Knowing these obstacles in advance lets you build a stronger claim from day one. The rideshare accident liability framework in California adds another layer of complexity, particularly around independent contractor status and platform liability.

For drivers who rely on their vehicles for income, vehicle damage coverage gaps during Period 1 create serious financial exposure that most do not anticipate until after an accident occurs.

How do you maximize your Uber or Lyft accident compensation?

Settlement valuations depend on policy limits, fault evidence, injury severity, and jurisdictional caps. Each of those variables requires active management, not passive waiting.

Verify app status and coverage limits first

Confirm in writing which period was active before you accept any settlement offer. A Period 1 claim and a Period 3 claim carry completely different maximum payouts. Accepting a Period 1 settlement when the driver was actually in Period 3 is an irreversible mistake.

Handle medical liens strategically

Lien resolution requires applying both contractual and statutory rules. Medicare liens, for example, carry federal priority and must be resolved before any settlement funds are disbursed. An attorney who specializes in rideshare claims can negotiate lien reductions that directly increase your net recovery.

Avoid premature settlements

Insurance adjusters move fast and make early offers that sound reasonable. Early offers almost never account for future medical costs, long-term disability, or lost earning capacity. Accepting one closes your claim permanently.

- Document every medical appointment, prescription, and therapy session.

- Get a written prognosis from your treating physician before agreeing to any settlement.

- Track all out-of-pocket expenses, including transportation to medical appointments.

- Keep a daily pain journal to document how the injury affects your life.

Pro Tip: If your injuries include whiplash or soft-tissue damage, do not settle until you reach maximum medical improvement (MMI). Settling before MMI means you cannot claim future treatment costs that have not yet been incurred.

| Compensation Factor | Why It Matters |

|---|---|

| Policy period confirmed | Determines the maximum available coverage limit |

| Medical lien resolution | Directly increases your net payout after settlement |

| Future medical costs | Must be calculated before any final settlement is signed |

| Comparative fault percentage | Reduces your recovery by your share of fault under California law |

| Structured settlement option | Provides long-term income for serious or permanent injuries |

Understanding how car accident compensation works in California gives you a clearer picture of what your claim is actually worth before you sit down with an adjuster.

Key Takeaways

A rideshare accident claim with Uber or Lyft requires identifying the correct insurance period, documenting app status immediately, and resolving medical liens before accepting any settlement offer.

| Point | Details |

|---|---|

| Insurance period controls coverage | The driver’s app status at impact determines whether $50,000 or $1,000,000 applies. |

| Period 1 is the riskiest gap | Personal policies often exclude coverage when the app is on but no trip is accepted. |

| Document app status immediately | A screenshot of the active trip is the strongest evidence against period disputes. |

| Lien resolution increases net recovery | Medicare, Medicaid, and hospital liens reduce your payout and must be negotiated. |

| Never settle before reaching MMI | Early settlements permanently close your claim and exclude future medical costs. |

What I have learned from handling rideshare claims in California

After more than two decades representing injured victims in the San Fernando Valley, I can tell you that rideshare accident claims are genuinely different from standard car accident cases. The insurance structure alone requires a level of technical analysis that most general practitioners are not prepared for.

The app-period dispute is the one that surprises victims most. I have seen insurers argue, with a straight face, that a driver was “between trips” when the platform’s own records showed an active booking. That kind of dispute does not resolve itself. It requires subpoenas, platform data requests, and sometimes federal court coordination. Victims who try to handle that process alone almost always lose the argument.

What I tell every client who comes to me after a rideshare accident is this: your first 48 hours determine the strength of your entire case. The evidence you collect, the statements you do not give, and the documentation you preserve in those two days matter more than anything that happens later. The insurance companies know this. Their adjusters call quickly because early contact produces cheaper settlements.

The lien issue is the other area where I see victims consistently underserved. A gross settlement of $200,000 can net a victim less than $80,000 after Medicare, Medicaid, and hospital liens are applied without negotiation. Proper lien resolution is not optional. It is the difference between a settlement that actually covers your losses and one that leaves you in debt.

Rideshare litigation is also evolving. Platforms are pushing arbitration clauses harder than ever, and courts are increasingly scrutinizing whether those clauses are enforceable in personal injury contexts. The legal landscape will continue to shift, and victims who understand their rights will be better positioned to assert them. You have more leverage than the initial settlement offer suggests.

— Matthew Nezhad

Oakslawfirm is ready to fight for your rideshare claim

Rideshare accident claims in California involve layered insurance, app-period disputes, and lien negotiations that require experienced legal representation. Oakslawfirm, founded by San Fernando Valley personal injury attorney Matthew Nezhad, has spent more than two decades securing maximum compensation for injured victims throughout California.

If you were injured in an Uber or Lyft accident, the next step is understanding your legal options before the insurance company makes its first move. Oakslawfirm offers a free case evaluation with no obligation. Learn how to file a personal injury lawsuit in Los Angeles and what the process looks like from start to finish. You can also reach the team directly through the free case evaluation page to get answers specific to your situation.

FAQ

What insurance covers a rideshare accident during an active trip?

During an active Uber or Lyft trip (Periods 2 and 3), primary commercial liability coverage of $1,000,000 applies. This coverage is primary, meaning it pays before any personal auto policy.

How do I prove the driver’s app was active at the time of the accident?

Screenshot your trip receipt immediately after the accident and request written confirmation of the driver’s app status from the platform. These two documents are the strongest evidence against insurer disputes over coverage periods.

Can I sue Uber or Lyft directly after an accident?

Direct lawsuits against Uber or Lyft are limited by their classification of drivers as independent contractors and by arbitration clauses in their terms of service. A rideshare accident lawyer can assess whether those clauses apply to your specific claim.

How long do I have to file a rideshare injury claim in California?

California’s statute of limitations for personal injury claims is generally two years from the date of the accident. Filing after that deadline typically bars your claim permanently, so acting promptly protects your rights.

What reduces my net settlement in a rideshare accident claim?

Medical and health plan liens from Medicare, Medicaid, ERISA plans, and hospitals are deducted from your settlement before you receive any funds. Proper lien negotiation by an attorney can significantly increase your net recovery.