After a car accident, you face one of the most consequential financial decisions of your life: accept a settlement or file a lawsuit. The car accident lawsuit vs settlement choice is not just procedural. It directly determines how much money you walk away with and how long you wait to get it. Most car accident cases resolve through settlement negotiations rather than trial, but “most” does not mean “always best.” Knowing which path fits your situation can mean the difference between covering your medical bills and falling short by tens of thousands of dollars.

Table of Contents

- Key takeaways

- Car accident lawsuit vs settlement: how each one works

- Key factors that push you toward settlement or lawsuit

- The process: from first claim to final resolution

- Common mistakes that cost accident victims money

- What to realistically expect in compensation

- My take after two decades in the courtroom

- How Oaks Law Firm can help you get the most from your claim

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Settlements resolve faster | Most cases close within months, while litigation can stretch from 6 months to over 3 years. |

| Policy limits cap what insurers pay | Insurers cannot offer more than the at-fault driver’s coverage, regardless of your actual damages. |

| First offers are rarely fair | Initial settlement offers are almost always low and negotiable with proper documentation. |

| Lawsuits can yield higher awards | When insurers undervalue serious injuries, a verdict or pre-trial settlement often exceeds the original offer. |

| Documentation is your leverage | Strong evidence of injury severity, liability, and financial losses strengthens both settlements and lawsuits. |

Car accident lawsuit vs settlement: how each one works

Before you can make the right call, you need to understand what you are actually choosing between.

What a settlement is. A car accident settlement is a negotiated agreement between you and an insurance company (or the at-fault driver) where you accept a specific dollar amount in exchange for releasing all future legal claims. Once you sign a release, the case is closed permanently. The process typically starts when you or your attorney files a claim with the at-fault party’s insurer, submits documentation of your injuries and losses, and enters into a back-and-forth negotiation with the claims adjuster.

The adjuster’s job is to pay you as little as the evidence will allow. They are not your advocate. They evaluate injury severity, medical records, lost wages, property damage, and fault evidence before making an offer. Insurers weigh all of this when deciding what to put on the table.

What a lawsuit is. Filing a car accident lawsuit means taking your claim to civil court. You sue the at-fault party directly, and the legal process unfolds through formal stages: pleadings, discovery, motions, and potentially a trial in front of a judge or jury. Critically, the majority of lawsuits still settle before reaching trial. Filing the lawsuit itself often signals to the insurer that you are serious, which can unlock a significantly better offer.

Here are the core differences between the two paths:

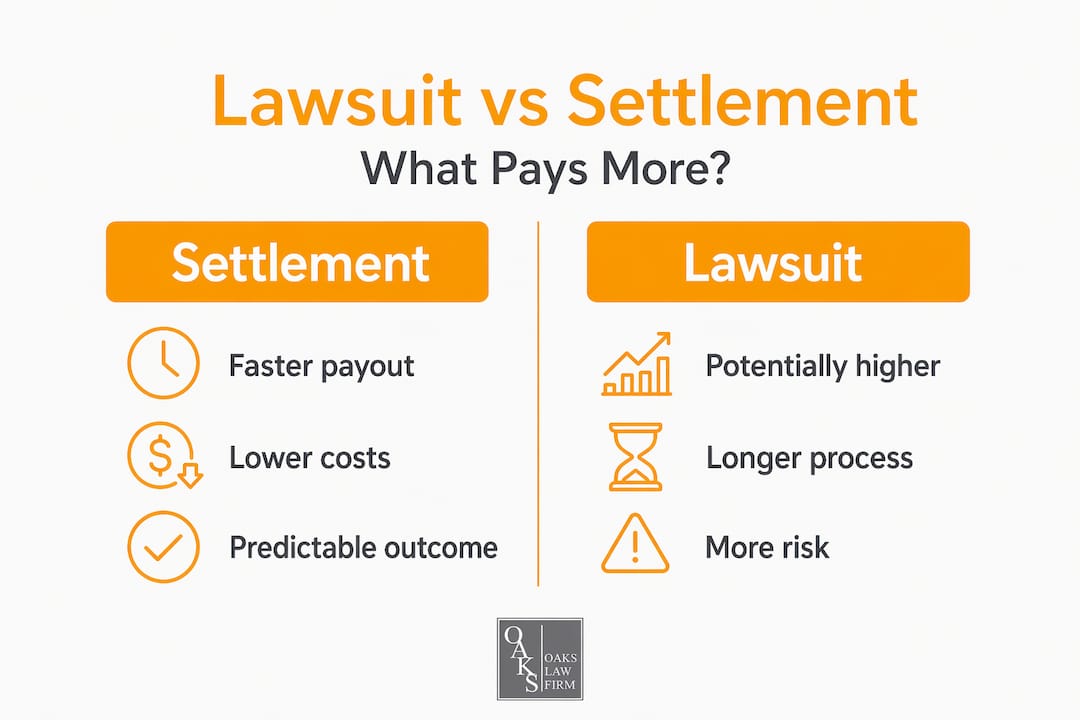

- Timeline. Settlements can close in weeks to months. Lawsuits typically take six months to three years or more.

- Certainty. A settlement gives you a guaranteed amount. A trial outcome depends on the jury.

- Cost. Litigation involves attorney fees, court costs, and expert witnesses. Settlements skip most of that.

- Privacy. Settlements stay out of public court records. Verdicts do not.

One thing many people do not realize: in no-fault insurance states, your right to sue is restricted to cases involving serious injury thresholds. California is a fault state, which means you have the option to pursue either path after a collision.

Pro Tip: Never accept or verbally agree to a settlement at the accident scene. A New Jersey court upheld an oral agreement made right after a crash as legally binding, which permanently barred the injured party from pursuing further compensation.

Key factors that push you toward settlement or lawsuit

This is where the real decision-making happens. Neither option is universally better. What matters is your specific situation.

1. Injury severity. Minor injuries like soft tissue strains or small cuts are strong candidates for settlement. The medical costs are predictable, recovery is usually complete, and the time and stress of litigation is hard to justify. Catastrophic injuries, including traumatic brain injuries, spinal cord damage, or permanent disability, are a different story. The long-term costs are enormous and sometimes unclear for months after the accident. Settling too quickly on a severe injury is one of the most expensive mistakes accident victims make.

2. Clarity of fault. When liability is obvious, like a rear-end collision caught on dashcam, insurers have less leverage to fight your claim. When fault is disputed, insurers use that uncertainty to justify low offers. A lawsuit forces the legal process of discovery, which can surface evidence that resolves the dispute in your favor.

3. Insurance policy limits. This one surprises people. Insurers can only offer up to the at-fault driver’s policy limits regardless of how severe your injuries are. If you have $200,000 in damages but the driver carries only $50,000 in liability coverage, the insurer’s maximum offer is $50,000. A lawsuit against the driver personally may recover more, but only if they have assets worth pursuing. Understanding how California compensation works before you negotiate protects you from leaving money on the table.

4. Strength of your evidence. Clear liability and documented evidence of your injuries increase both your settlement leverage and your trial prospects. Medical records, police reports, witness statements, and photos from the scene all contribute to a stronger position whether you settle or sue.

5. Your personal circumstances. Do you need money quickly to cover ongoing medical bills? A settlement may be your best move. Are you financially stable enough to wait 12 to 24 months for a potential higher jury award? Then litigation might be worth exploring. Your risk tolerance matters here too. Trials carry real uncertainty. A jury could award more than the settlement offer, or they could award less.

6. Cost and stress of litigation. Lawsuits are exhausting. Depositions, court appearances, waiting periods, and the emotional weight of reliving the accident take a real toll. Litigation may yield higher awards but comes with higher fees and longer durations. That tradeoff is real and personal.

Pro Tip: Get a full medical evaluation and a projected treatment plan from your doctor before accepting any offer. You cannot renegotiate a settlement after you have signed the release, even if your condition worsens significantly.

The process: from first claim to final resolution

Whether you settle or sue, the process follows a predictable sequence. Knowing each stage helps you make informed decisions along the way.

Stage 1: Filing your initial claim

Report the accident to your own insurer, then file a claim against the at-fault driver’s insurance. Provide the police report, photos, medical records, and any witness contact information. The insurer assigns an adjuster who begins evaluating your claim.

Stage 2: Settlement offer and negotiation

The adjuster will make an initial offer. That first number is almost always low. Initial offers frequently fall short of covering actual medical costs, let alone lost wages or pain and suffering. You have the right to counter with documentation: itemized medical bills, employer statements confirming lost income, and written opinions from treating physicians about long-term care needs.

Effective negotiation is not about emotion. It is about evidence. The more documentation you can point to, the harder it is for the adjuster to justify a low number.

Stage 3: Deciding whether to sue

If negotiations stall or the insurer refuses to offer a fair amount, your attorney files a lawsuit before the statute of limitations expires. In California, you generally have two years from the date of the accident to file. Missing that deadline ends your case permanently.

Stage 4: Lawsuit stages

Here is a clear comparison of what each path looks like once you are in the legal process:

| Stage | Settlement path | Lawsuit path |

|---|---|---|

| Initial filing | Claim filed with insurer | Complaint filed with court |

| Evidence exchange | Informal document submission | Formal discovery process |

| Negotiation | Direct with adjuster or attorney | Often continues during litigation |

| Resolution timing | Weeks to months | 6 months to 3+ years |

| Resolution certainty | Guaranteed agreed amount | Jury verdict or judge ruling |

| Costs | Lower, minimal legal fees | Higher, expert witness fees possible |

Most lawsuits in California settle during or after the discovery phase, once both sides have seen each other’s full evidence. Filing a lawsuit does not mean you are committed to trial. It means you are committed to getting fair compensation.

Pro Tip: Having an attorney handle dealing with car insurers significantly changes the outcome. Studies consistently show represented claimants receive higher settlements than those who negotiate alone.

What changes when you have legal representation

Attorneys who specialize in personal injury cases know how insurers calculate offers and where the leverage points are. They also handle all communication, which protects you from inadvertently saying something that reduces your claim. If you want to understand how to file a personal injury lawsuit in California, the process involves specific procedural requirements that are easy to get wrong without guidance.

Common mistakes that cost accident victims money

Most of the errors people make in this process come down to moving too fast or not knowing what they do not know.

- Accepting the first offer without negotiating. This is the single most common and costly mistake. Insurers bank on victims being unaware that the first offer is a starting point, not a final number.

- Settling before knowing your full medical picture. If your doctor has not completed your treatment or provided a long-term prognosis, you do not have a complete picture of your damages. Settling prematurely locks in a number that may not cover future costs.

- Missing the statute of limitations. California gives you two years from the accident date to file a lawsuit. If you let that deadline pass while waiting on settlement talks, you lose all legal leverage.

- Undervaluing non-economic damages. Pain and suffering, emotional distress, and loss of enjoyment of life are compensable in California. These can exceed economic damages in serious injury cases, yet many victims do not include them in their demands.

- Failing to document consistently. Keep every medical receipt, every prescription, every missed workday. A journal documenting your daily pain, physical limitations, and emotional impact can support a pain and suffering claim meaningfully.

- Ignoring policy limits gaps. If the at-fault driver is underinsured, your own underinsured motorist coverage may fill the gap. Many people do not know to claim it.

Pro Tip: California law allows you to claim compensation for both past and future medical expenses. Ask your physician to provide a written estimate of expected future treatment costs before finalizing any settlement negotiation.

What to realistically expect in compensation

Compensation varies widely depending on the specifics of your case, but data gives you a reasonable framework for expectations.

Average car accident settlements run approximately $30,416 overall, but that average masks enormous variation. Minor injury cases typically settle between $3,000 and $25,000. Moderate injuries involving surgery, extended physical therapy, or partial disability land between $25,000 and $150,000. Catastrophic injuries, including permanent disability or severe brain trauma, can exceed $500,000 and reach into the millions.

The math behind any settlement or verdict includes two categories of damages:

Economic damages are the concrete, calculable losses: medical bills (past and future), lost wages, reduced earning capacity, vehicle repair or replacement, and out-of-pocket expenses. These are proven with receipts and records.

Non-economic damages cover the human cost of the injury. Pain and suffering, emotional distress, loss of consortium, and reduced quality of life fall here. These are harder to quantify, which is exactly why insurers push back on them hardest. California does not cap non-economic damages in car accident cases, unlike some other states.

When lawsuits produce outcomes that exceed settlement offers, it is usually because a jury assigned significant non-economic damages that the insurer refused to fairly value. Settlements may avoid trial costs but can leave non-economic compensation significantly underpaid. Understanding average LA settlement amounts by injury type can help you benchmark whether what you have been offered reflects reality.

Timing affects more than just patience. Waiting for a trial verdict can take years, during which your bills continue accumulating. Some clients are better served by a solid settlement than by waiting for a higher number that may never come. Others, particularly those with severe injuries and strong evidence, are underserved by settling fast.

My take after two decades in the courtroom

I have handled car accident cases in California for over two decades, and the question I hear most often is some version of: “Should I just take the settlement and be done with it?”

My honest answer is: it depends, but not in the way most people expect. The cases where I have seen clients regret settling quickly were almost always ones involving ongoing or worsening injuries where the full cost was not yet clear. One client settled within three months of a rear-end collision, convinced her neck pain was temporary. Two years later, she needed cervical surgery that cost far more than her entire settlement. That is a permanent financial loss she could not undo.

On the other side, I have seen clients dig in for trials on cases where the evidence was weaker than they believed. The jury sided with the insurer, and they walked away with less than the original offer, plus two years of stress. The evidence, not the emotion, should drive the decision.

What I tell every client is this: do not decide until your medical picture is complete. Do not negotiate without knowing what your damages actually are. And do not assume that filing a lawsuit means going to trial. Most lawsuits I have filed settled before a jury ever heard the case, often at significantly higher amounts than the pre-suit offer.

The one piece of advice I give everyone regardless of their situation: document everything from day one. A photo taken at the scene, a journal entry written the night of the accident, a follow-up visit to your doctor the next morning. These details are the raw material of a strong claim, in settlement or in court.

— Matthew Nezhad

How Oaks Law Firm can help you get the most from your claim

At Oaks Law Firm, we work with car accident victims throughout the San Fernando Valley and across California who are trying to make exactly this decision. Matthew Nezhad and his team have spent over two decades evaluating whether clients are better served by negotiating a settlement or building a lawsuit. There is no one-size-fits-all answer, which is why the initial consultation matters so much.

We handle passenger injury claims, cases involving uninsured or underinsured drivers, and serious injury cases where insurers have made offers that do not come close to covering real losses. Our no fee guarantee means you pay nothing unless we win. There is zero financial risk in getting a professional evaluation of your case.

If you are wondering whether the offer you have received is fair, or whether your situation warrants filing a lawsuit, contact Oaks Law Firm for a free case evaluation. The conversation costs you nothing and could be the most valuable hour you spend after your accident.

FAQ

What is the main difference between a car accident settlement and a lawsuit?

A settlement is a negotiated agreement between you and the insurer that closes your case in exchange for a set payment. A lawsuit takes your claim to court where a judge or jury determines compensation, a process that typically takes far longer but can yield a higher award.

Should I settle after a car accident or go to court?

Settling is often the better choice for minor to moderate injuries where medical costs are predictable and liability is clear. A lawsuit makes more sense when the insurer is significantly undervaluing a serious injury, when liability is disputed, or when damages clearly exceed what the insurer is willing to offer.

How long does a car accident lawsuit take compared to a settlement?

Settlements often resolve within a few months of filing a claim. Lawsuits typically take six months to three years or longer depending on case complexity, court schedules, and whether the case goes to trial.

What is the average settlement amount for a car accident?

The overall average settlement runs approximately $30,416, though minor injuries may settle between $3,000 and $25,000, while catastrophic injuries can exceed $500,000 depending on the severity and long-term impact.

Can I still negotiate after receiving a settlement offer?

Yes. Initial settlement offers are typically low and intended as a starting point. You can counter with medical documentation, expert opinions, and evidence of lost wages. An attorney can significantly strengthen your negotiating position.