A commercial vehicle accident claim is a formal legal process where an injured party seeks compensation after an accident involving a vehicle used for business purposes. These claims are governed by a distinct set of federal regulations, higher insurance limits, and more complex liability rules than standard personal vehicle claims. Understanding how this process works gives you a real advantage when dealing with insurance carriers and corporate legal teams that move fast.

Disclaimer: This article provides general information only. Your specific case facts, jurisdiction, and circumstances may produce different outcomes. Consult a licensed attorney for advice tailored to your situation.

What is a commercial vehicle accident claim?

A commercial vehicle accident claim is the legal mechanism through which an injured person recovers damages after a crash involving a business-operated vehicle. The term “commercial vehicle accident claim” is the everyday phrase most people search for. The recognized industry term is a commercial motor vehicle (CMV) liability claim, and both refer to the same process under federal and state law.

These claims differ from personal auto claims in three fundamental ways: the vehicles involved carry much higher insurance minimums, multiple parties can share legal liability, and federal Department of Transportation regulations apply to the vehicles and their operators. That combination makes commercial claims significantly more complex and potentially more valuable than a standard fender-bender claim.

Oakslawfirm has handled these cases throughout the San Fernando Valley and California for over two decades. The firm’s experience shows that claimants who understand the process early recover more and make fewer costly mistakes.

What qualifies as a commercial vehicle and why does it matter?

The classification of a vehicle as “commercial” directly determines which insurance rules, liability standards, and federal regulations apply to your claim. Getting this classification right is the first step in building a strong case.

The Federal Motor Carrier Safety Administration (FMCSA) defines a commercial motor vehicle as any vehicle used in interstate commerce that meets one of the following criteria:

- Gross vehicle weight rating (GVWR) of 10,001 pounds or more

- Designed to transport 9 or more passengers for compensation

- Designed to transport 16 or more passengers regardless of compensation

- Used to transport hazardous materials in quantities requiring placards

Common examples include semi-trucks, tractor-trailers, delivery vans, box trucks, tanker trucks, and company-owned passenger vehicles used for business travel. A rideshare vehicle operating on a commercial platform can also qualify under certain state rules.

The classification matters because it triggers a separate legal and regulatory framework. FMCSA rules govern driver hours of service, vehicle maintenance logs, and cargo loading standards. California adds its own layer of oversight through the California Highway Patrol (CHP) commercial vehicle inspection program. When a driver or company violates these regulations, those violations become direct evidence of negligence in your claim.

Federal and state regulations add layers of complexity to commercial cases. Understanding employer liability for negligent practices is critical to maximizing your compensation potential.

How does a commercial vehicle accident claim differ from a personal vehicle claim?

The core difference is the number of parties who can be held legally responsible. In a personal vehicle accident, liability typically falls on one driver. In a commercial vehicle case, liability often extends beyond the driver to employers, cargo loaders, and maintenance contractors, creating complex legal scenarios.

That expanded liability pool changes everything about how a claim is investigated and negotiated. Here is how the differences play out in practice:

-

Multiple liable parties. The trucking company may be liable for negligent hiring or scheduling. A third-party cargo loader may share fault if improper loading caused the crash. A maintenance contractor may be responsible if brake failure contributed to the collision.

-

Higher insurance limits. Commercial carriers hold high liability limits starting at $750,000 federally, often $1 million or more. That means larger potential settlements, but also more aggressive defense.

-

Rapid-response insurance teams. Adjusters typically begin their investigation while the injured party is still hospitalized. These teams work to build a defense before you have gathered your own evidence.

-

Longer timelines. Simple commercial claims can close in 30–90 days. Complex cases involving serious injuries, disputed liability, or multiple defendants routinely take 12–36 months to resolve.

-

Regulatory investigation records. FMCSA logs, driver qualification files, electronic logging device (ELD) data, and vehicle inspection reports all become part of the evidence record. Personal vehicle claims have no equivalent documentation layer.

Pro Tip: Contact a commercial vehicle attorney before speaking with any insurance adjuster. Corporate carriers have legal teams working from day one. You should too.

The truck accident liability picture in commercial cases is rarely simple. Knowing who to name in a claim, and why, directly affects how much you recover.

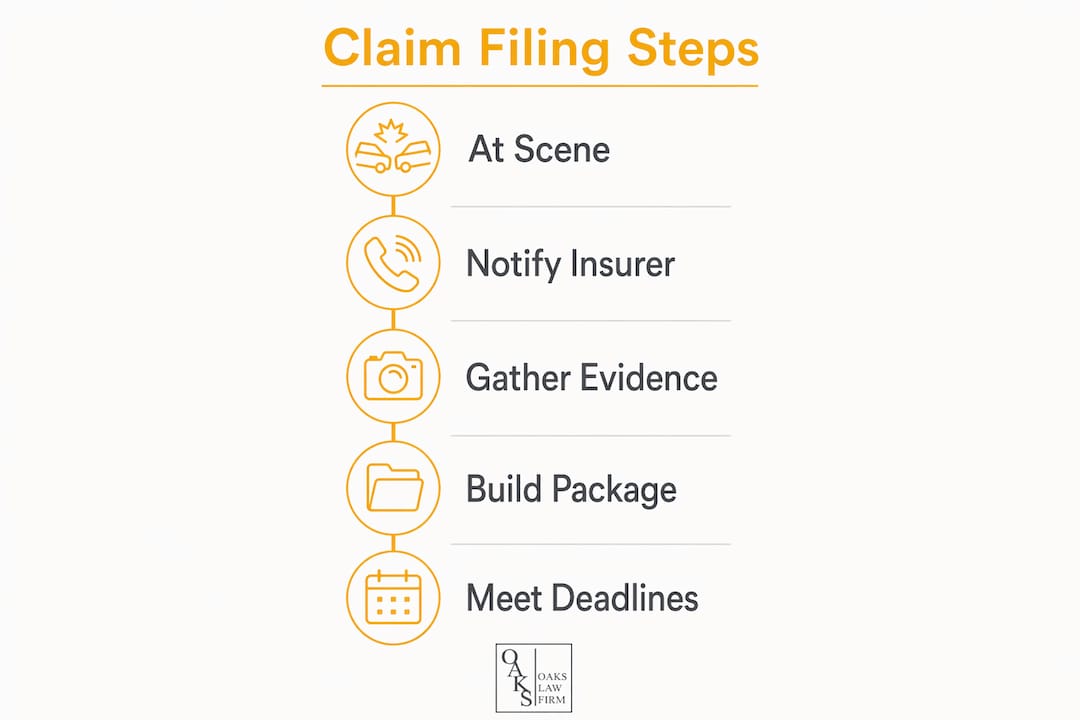

How to file a commercial vehicle accident claim: step by step

Filing a commercial accident claim correctly from the start protects your right to full compensation. Mistakes made in the first 48 hours are often the hardest to fix later.

At the accident scene

Document everything before vehicles are moved. Take photos of all vehicles, license plates, DOT numbers displayed on commercial vehicles, road conditions, skid marks, and any visible injuries. Collect the driver’s commercial license number, employer name, and insurance carrier information. Do not admit fault or make statements about how you feel physically. Adrenaline masks pain, and early admissions can damage your claim.

Notify your insurer within 24–48 hours

Notifying your insurer within 24–48 hours after an incident is critical to avoid coverage denial due to “late notice” clauses. Many commercial policies contain strict provisions that trigger automatic denial if notification is delayed. Report the accident factually and briefly. Do not speculate about fault or describe injuries in detail at this stage.

Build your demand package

The most critical document in the claim process is the demand package. A thorough demand package includes police reports, medical documentation, lost wages proof, and future treatment narratives. Thorough early documentation limits the insurer’s ability to undervalue or deny your claim.

Your demand package should include:

- Police and accident reports from all responding agencies

- Medical records and bills covering all treatment from the date of the accident forward

- Proof of lost wages such as pay stubs, employer letters, or tax records

- Future treatment estimates from your treating physicians

- Photos and video from the scene and of your injuries over time

- Witness statements collected as close to the accident date as possible

- FMCSA and ELD records obtained through formal discovery or preservation letters

Know your legal deadlines

| Jurisdiction | Injury claim deadline | Insurer acknowledgment | Insurer acceptance or denial |

|---|---|---|---|

| California | 2 years from accident date | Not specified by statute | Reasonable time standard |

| Texas | 2 years from accident date | 15 business days | 15 business days after documentation |

| Federal (FMCSA claims) | Varies by claim type | N/A | N/A |

In Texas, insurance companies must acknowledge claims within 15 days and accept or deny them within 15 business days after documentation submission. California operates under a similar good-faith standard. Missing your state’s statute of limitations ends your right to sue entirely.

Pro Tip: Send a preservation letter to the trucking company within days of the accident. This legally requires them to retain ELD data, maintenance logs, and driver records that are often deleted on routine schedules.

Track your claim’s progress in writing. Every phone call with an adjuster should be followed by a confirming email. Written records protect you if the insurer later disputes what was agreed.

Common challenges when navigating a commercial vehicle accident claim

Commercial vehicle claims attract well-funded opposition. Knowing the tactics insurers use gives you a real chance to counter them.

Aggressive defense teams move immediately. Adjusters begin building their case while you are still in the hospital. They photograph the scene, interview witnesses, and download vehicle data before you have retained an attorney. This head start is intentional.

Recorded statements are a trap. Recorded statements taken soon after accidents are often used by insurers to minimize claims. Early statements made without full medical information can reduce your claim’s value significantly. Wait until you have complete medical documentation and legal counsel before giving any recorded statement.

Denial tactics are common. Insurers may argue the driver was an independent contractor rather than an employee, shifting liability. They may claim the cargo loader was a separate company. They may dispute the severity of your injuries by pointing to gaps in treatment. Each of these tactics requires a specific counter-strategy backed by documentation.

Loss Run records carry long-term costs. Small claims may lead to premium surcharges over 3–5 years, sometimes costing more than the claim payout itself. If you operate a commercial vehicle yourself and are filing against your own policy for a minor incident, weigh the long-term premium impact before filing.

Documenting injuries properly from the moment of the accident is one of the most effective defenses against insurer denial tactics. Gaps in medical records are the most common reason insurers reduce settlement offers.

What types of compensation can you expect from a commercial vehicle accident claim?

Commercial vehicle accident compensation covers both economic and non-economic damages. The amount you recover depends on injury severity, liability clarity, and the strength of your documentation.

| Damage type | What it covers | Typical evidence required |

|---|---|---|

| Medical expenses | Hospital bills, surgery, therapy, future care | Medical records, physician estimates |

| Lost wages | Income lost during recovery | Pay stubs, employer letters, tax returns |

| Pain and suffering | Physical pain and emotional distress | Medical records, personal journal, testimony |

| Property damage | Vehicle repair or replacement | Repair estimates, photos, market value data |

| Wrongful death | Funeral costs, lost financial support | Death certificate, financial records |

Approximately 95% of commercial vehicle accident cases resolve through settlement outside of court. Simple claims close in 30–90 days, while complex cases take 12–36 months. That statistic matters because it tells you negotiation, not trial, is where most outcomes are decided.

Settlement values vary widely. Rear-end collision settlements in commercial cases range from $150,000 to $200,000. Fatal crashes can carry an economic impact of $3.6 million or more. Injury severity, the number of liable parties, and the quality of your documentation all drive the final number.

The car accident compensation framework in California allows recovery for both economic and non-economic damages. Understanding which categories apply to your injuries is the foundation of a strong demand package.

Key takeaways

A commercial vehicle accident claim is one of the most legally complex injury claims you can file, and the outcome depends heavily on how quickly and thoroughly you act in the first days after the accident.

| Point | Details |

|---|---|

| Classification drives the claim | Vehicles meeting FMCSA weight or passenger thresholds trigger federal regulations and higher insurance limits. |

| Multiple parties share liability | Employers, cargo loaders, and maintenance contractors can all be named in a commercial vehicle claim. |

| Notify your insurer within 48 hours | Late notice clauses can void coverage entirely, so report the accident immediately and in writing. |

| Build a complete demand package | Police reports, medical records, lost wages proof, and future treatment estimates are all required for a strong claim. |

| Most cases settle out of court | Around 95% of commercial vehicle claims resolve through negotiation, making documentation and legal strategy the deciding factors. |

What I have learned after years of commercial vehicle cases

By Matthew Nezhad

The single biggest mistake I see injured people make is waiting. They wait to see a doctor. They wait to call an attorney. They wait to gather evidence. By the time they act, the trucking company has already downloaded the truck’s black box data, interviewed the driver, and built a narrative that minimizes their liability.

Commercial vehicle cases are not like standard car accident claims. The other side has professionals working the case from the moment the crash happens. Their adjusters are experienced, their attorneys are specialized, and their goal is to pay you as little as possible. That is not cynicism. That is the business model.

What I have found actually works is preparation and speed. Preserve evidence before it disappears. Get medical treatment immediately and keep every record. Do not give recorded statements before you understand the full picture of your injuries. And do not sign any release until you know the long-term cost of your injuries, because once you sign, the case is closed.

The clients who recover the most are the ones who treat their claim like a serious legal matter from day one. They document everything, they follow medical advice, and they get legal counsel before making decisions that cannot be undone. The California truck accident process has specific deadlines and procedural requirements that can permanently affect your rights if missed.

One more thing: do not let the size of the insurance company intimidate you. High policy limits mean there is real money available for your recovery. The question is whether you are positioned to claim it.

— Matthew Nezhad

Oakslawfirm is ready to fight for your commercial vehicle claim

If you were injured in an accident involving a commercial vehicle, the legal process ahead is more complex than a standard car accident case. Oakslawfirm has spent over two decades protecting injured victims throughout the San Fernando Valley and California, including cases involving semi-trucks, delivery vehicles, and company-operated cars.

Attorney Matthew Nezhad and his team know how to counter aggressive insurance defense tactics, preserve critical evidence, and build demand packages that hold up under scrutiny. Oakslawfirm accepts a limited number of cases each year, which means every client gets focused attention. The firm operates on a no-fee guarantee policy, so you pay nothing unless your case wins. Contact Oakslawfirm today for a free case evaluation and find out exactly where you stand.

FAQ

What is a commercial vehicle accident claim?

A commercial vehicle accident claim is a formal legal process where an injured person seeks compensation after a crash involving a vehicle used for business purposes. These claims involve higher insurance limits, federal regulations, and often multiple liable parties.

How long do I have to file a commercial vehicle accident claim in California?

California law gives you two years from the date of the accident to file a personal injury claim. Missing this filing deadline permanently eliminates your right to sue.

Who can be held liable in a commercial vehicle accident?

Liability can extend to the driver, the employing company, cargo loaders, and maintenance contractors. Negligent hiring or scheduling practices by employers are frequently central to litigation and settlement negotiations.

Should I give a recorded statement to the insurance company?

No. Recorded statements taken shortly after an accident are routinely used by insurers to reduce claim value. Wait until you have complete medical documentation and have consulted an attorney before giving any statement.

How much is a commercial vehicle accident claim worth?

Settlement amounts vary based on injury severity, liability, and documentation quality. Rear-end commercial vehicle settlements commonly range from $150,000 to $200,000, while fatal crash cases can carry economic impacts exceeding $3.6 million.