Getting hit by an uninsured driver in California means your own uninsured motorist (UM) coverage is typically your fastest path to compensation. This is the standard industry term for the protection that pays your medical bills, lost wages, and pain and suffering when the at-fault driver carries no insurance. California law also gives you the right to sue that driver directly, though collecting is rarely simple. Knowing what happens if you get hit by an uninsured driver in California, and acting quickly, is the difference between full recovery and leaving money on the table. The California DMV, your insurance company, and a two-year legal deadline all enter the picture from day one.

What happens if you get hit by an uninsured driver in California?

Your own UM coverage steps in as the primary source of payment when the at-fault driver has no insurance. Your insurer pays up to your policy limits for injuries and, if you added uninsured motorist property damage (UMPD) coverage, for vehicle repairs too. This happens even though the other driver caused the crash. The speed of that payment is the main reason UM coverage matters so much.

California law does not make UM coverage mandatory for drivers. However, insurers must offer it every time you purchase an auto policy in the state. You can decline it in writing, but doing so removes your strongest financial safety net. If you are unsure whether you accepted UM coverage, call your insurer today and ask for a declarations page.

Beyond your own policy, California tort law gives you the right to file a lawsuit against the uninsured driver for the full value of your damages. That legal right exists regardless of whether you carry UM coverage. The practical challenge is that drivers without insurance often lack the assets to pay a judgment. Your two main tools are your own policy and the courts, and most victims use both.

How does uninsured motorist coverage work in California?

Uninsured motorist coverage in California splits into two types: UM bodily injury (UMBI) and UM property damage (UMPD). UMBI pays for medical expenses, lost wages, rehabilitation costs, and pain and suffering. UMPD covers damage to your vehicle when the at-fault driver is uninsured, though it typically carries a $250 deductible. Underinsured motorist (UIM) coverage is a separate but related product. UIM applies when the at-fault driver has some insurance but not enough to cover your full losses.

Here is what UM coverage can pay for:

- Medical bills: Emergency care, surgery, physical therapy, and follow-up treatment

- Lost wages: Income you missed while recovering from your injuries

- Pain and suffering: Compensation for physical pain and emotional distress

- Property damage: Vehicle repairs or replacement if you added UMPD to your policy

- Future medical costs: Ongoing treatment expenses tied directly to the accident

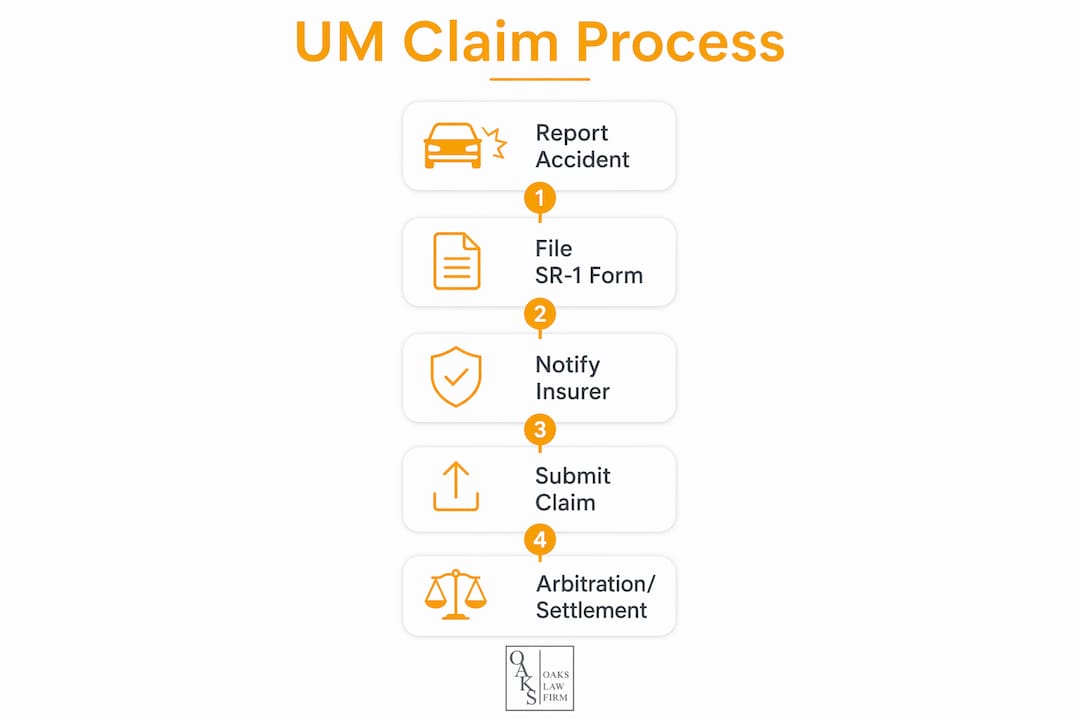

Filing a UM claim works differently from a standard liability claim. You file against your own insurer, not the at-fault driver’s company. Your insurer then steps into the shoes of the uninsured driver and evaluates the claim. Disputes over the value of your claim go to binding arbitration rather than a jury trial. That arbitration process is governed by your policy terms, so reading those terms before you file matters.

Pro Tip: Request a copy of your full policy, not just the summary, before your first call with your insurer. The arbitration clause and coverage limits are buried in the full document, and knowing them before negotiations start gives you a real advantage.

UIM coverage activates only after you exhaust the at-fault driver’s policy limits. If the other driver carries $15,000 in liability coverage and your damages total $80,000, UIM pays the gap up to your UIM limit. Stacking UM and UIM coverage on multiple vehicles is allowed in California and can significantly increase your total available protection.

Can you sue an uninsured driver in California?

California law gives accident victims the full right to sue an uninsured driver for damages. California Civil Code and tort law place no cap on damages when the victim carried valid insurance at the time of the crash. That means you can pursue medical costs, lost income, property damage, and pain and suffering through the courts.

The two-year deadline you cannot miss

California Code of Civil Procedure Section 335.1 sets a two-year statute of limitations for personal injury lawsuits. The same two-year window applies to initiating formal UM arbitration proceedings. Miss that deadline and you forfeit your claim entirely. The clock starts on the date of the accident, not the date you discovered your injuries. Check your California car accident deadline early and do not assume you have more time than you do.

How Proposition 213 limits your recovery

Proposition 213 is a California law that restricts damages for uninsured victims. If you lacked valid insurance at the time of the accident, you cannot recover non-economic damages like pain and suffering, even if the other driver was entirely at fault. You can still recover medical bills and lost wages, but the pain and suffering component disappears. This rule applies whether you sue the driver or file a UM claim. Carrying valid insurance protects your right to full compensation.

When suing makes sense vs. relying on insurance

Deciding whether to sue depends on the uninsured driver’s financial situation. Consider these factors before filing:

- Asset check: Does the driver own real property, a business, or other assets a judgment could attach to?

- Wage garnishment: California courts can order wage garnishment to satisfy a judgment over time.

- Policy limits: If your UM coverage is low, a lawsuit may recover damages your policy cannot reach.

- Time and cost: Litigation takes months or years and costs money, even on contingency.

- Settlement leverage: Filing a lawsuit often motivates uninsured drivers to negotiate a payment plan.

| Scenario | Best approach |

|---|---|

| Driver has no assets or income | Rely on UM coverage; lawsuit unlikely to yield payment |

| Driver owns property or earns steady wages | Lawsuit plus UM claim maximizes recovery |

| Your UM limits are low | Pursue both lawsuit and UM claim simultaneously |

| You lacked insurance at time of crash | Lawsuit for economic damages only; UM claim unavailable |

Suing an uninsured driver and filing a UM claim are not mutually exclusive. Many California victims pursue both at the same time. An attorney can coordinate both tracks so they do not interfere with each other.

What to do immediately after an accident with an uninsured driver

The actions you take in the first 24–72 hours after a California car accident with an uninsured driver directly affect the value of your claim. Gaps in documentation give insurers grounds to reduce or deny payment. Follow these steps without delay.

- Call 911: A police report creates an official record of the crash, the other driver’s identity, and the absence of insurance. A police report is one of the strongest pieces of evidence you can have for both a UM claim and a lawsuit.

- Document the scene: Photograph every vehicle, all visible damage, skid marks, road conditions, and any injuries. Video is better than photos alone.

- Collect witness information: Names and phone numbers from bystanders can corroborate your account if the other driver disputes fault.

- Seek medical care immediately: Go to an emergency room or urgent care clinic the same day, even if you feel fine. Delayed treatment creates gaps insurers use to argue your injuries were not caused by the crash.

- Notify your insurer promptly: Report the accident to your own insurance company as soon as possible. Most policies require prompt notification as a condition of UM coverage.

- Report to the California DMV: California law requires you to notify the Department of Motor Vehicles within 10 days of any collision involving injury or property damage over $1,000.

- Preserve all records: Keep every medical bill, repair estimate, prescription receipt, and pay stub showing missed work.

Pro Tip: Do not give a recorded statement to any insurance company, including your own, before speaking with an attorney. Adjusters are trained to ask questions that minimize your claim. A single poorly worded answer can reduce your payout significantly.

The DMV reporting requirement catches many drivers off guard. Filing the SR-1 form with the California DMV within 10 days is your legal obligation. Failure to file can result in license suspension. You can download the SR-1 form directly from the California DMV website.

How insurance claims and subrogation work after an uninsured accident

Filing a UM claim against your own insurer is not the same as filing a liability claim against the at-fault driver’s insurer. The table below shows the key differences.

| Factor | UM claim (your insurer) | Liability claim (at-fault driver’s insurer) |

|---|---|---|

| Who you file against | Your own insurance company | The at-fault driver’s insurer |

| Dispute resolution | Binding arbitration | Negotiation or lawsuit |

| Speed of payment | Generally faster | Depends on at-fault insurer cooperation |

| Deductible | May apply for UMPD | None for bodily injury claims |

| Availability | Only if you purchased UM coverage | Only if driver has liability insurance |

Subrogation is the process by which your insurer recovers the money it paid you by pursuing the uninsured driver directly. Your insurer may sue the at-fault driver to recoup its payment, and if successful, that recovery can include reimbursing your deductible. This means you may get your deductible back even if you never personally sue the other driver.

Filing a UM claim does not automatically raise your premiums in California. State law prohibits insurers from raising rates solely because you filed a UM claim when you were not at fault. However, if your insurer disputes fault or the circumstances are unclear, document everything carefully to protect your rate. Disputes over UM claim value go to arbitration, not court, so having organized records and medical documentation is your strongest negotiating tool. Learn more about how car accident compensation is calculated in California to understand what your full claim may be worth.

Key Takeaways

Being hit by an uninsured driver in California requires you to act fast, file a UM claim with your own insurer, report the crash to the DMV within 10 days, and preserve your right to sue before the two-year deadline expires.

| Point | Details |

|---|---|

| UM coverage is your fastest recovery | Your own uninsured motorist policy pays medical bills, lost wages, and pain and suffering up to your limits. |

| Two-year deadline is firm | California Code of Civil Procedure Section 335.1 gives you exactly two years to file or arbitrate. |

| Proposition 213 penalizes uninsured victims | Driving without insurance at the time of the crash eliminates your right to pain and suffering damages. |

| Subrogation can recover your deductible | Your insurer may pursue the at-fault driver and return your deductible if it wins. |

| Police report and DMV filing are required | Call 911 at the scene and file the SR-1 form with the California DMV within 10 days. |

What I have learned from years of uninsured motorist cases in California

After more than two decades handling personal injury cases in the San Fernando Valley, the pattern I see most often is this: victims wait too long and document too little. They assume their insurer will handle everything fairly, and they skip the police report because the other driver seems cooperative at the scene. By the time they call me, weeks have passed, the other driver has changed their story, and the medical records have gaps.

The uncomfortable truth about uninsured motorist claims in California is that your own insurer is not automatically on your side. Insurers have a financial interest in paying as little as possible, even on UM claims. I have seen adjusters use a delayed doctor visit, an inconsistent statement, or a missing receipt to cut a legitimate claim by thousands of dollars. The adversarial dynamic does not disappear just because you are filing against your own policy.

What actually works is treating your UM claim with the same seriousness as a lawsuit from day one. That means a police report, same-day medical care, a written timeline of events, and no recorded statements without legal advice. It also means understanding Proposition 213 before you assume you have full rights. Drivers who let their own insurance lapse, even briefly, can lose their right to pain and suffering damages entirely. That is a consequence most people do not learn about until it is too late.

My advice is to consult an attorney before you give your insurer a recorded statement. That one step costs you nothing and protects you from the most common mistake I see in these cases. If the other driver was uninsured, you are already dealing with a difficult situation. Do not make it harder by going it alone against a trained adjuster.

— Matthew Nezhad

How Oakslawfirm can help after an uninsured driver accident

Oakslawfirm has spent more than two decades fighting for accident victims across the San Fernando Valley and throughout California. Attorney Matthew Nezhad and his team handle uninsured and underinsured driver claims with the same intensity they bring to every case, because victims of uninsured drivers deserve full compensation, not a reduced settlement.

Oakslawfirm accepts a limited number of cases each year, which means every client receives direct attention from an experienced attorney. The firm operates on a no-fee guarantee policy: you pay nothing unless your case wins. If you were hit by an uninsured driver in California, contact Oakslawfirm today for a free case evaluation and find out exactly what your claim is worth before you speak with any insurance adjuster. You can also learn more about filing a personal injury lawsuit in Los Angeles to understand every option available to you.

FAQ

Does California require drivers to carry uninsured motorist coverage?

California does not require drivers to carry UM coverage, but insurers must offer it with every auto policy sold in the state. You must decline it in writing if you do not want it.

How long do I have to file a claim after being hit by an uninsured driver in California?

You have two years from the date of the accident to file a personal injury lawsuit or initiate UM arbitration under California Code of Civil Procedure Section 335.1. Missing this deadline forfeits your claim.

Will filing a UM claim raise my insurance rates in California?

California law prohibits insurers from raising your premium solely because you filed a UM claim when you were not at fault. Document the other driver’s lack of insurance clearly to protect your rate.

What if I was also uninsured at the time of the crash?

You can still sue the at-fault driver for economic damages like medical bills and lost wages. However, Proposition 213 bars uninsured victims from recovering non-economic damages like pain and suffering.

Can my insurer recover my deductible from the uninsured driver?

Yes. Through subrogation, your insurer can pursue the at-fault driver directly, and any recovery it obtains can include reimbursing your deductible.